While you can’t control what the markets will do next, you can get a handle on how much risk you’re comfortable taking with your investments. Discussing these three questions with your advisor can help

IF YOU’VE EVER WONDERED how you’d deal with a challenging market, the first few months of 2020 likely put that to the test. Between February and March of 2020, stocks plunged nearly 34%, shaking many investors’ faith in their investment strategy and financial futures.

“Markets can change very quickly and unexpectedly, and we cannot control that,” says Niladri Mukherjee, head of CIO Portfolio Strategy, Chief Investment Office, Merrill and Bank of America Private Bank. “What we can control is how we manage risk.”

The key is understanding your comfort with risk before a crisis hits, so you’re less tempted to pull out of the market when volatility strikes and miss out on potential gains when it recovers.

The following questions can help guide you in understanding how much risk you can tolerate — and afford — in any market.

How much risk can you take on and still sleep at night?

The dramatic drop in stock prices triggered by the coronavirus in early 2020 and the economic shutdown that followed can provide a useful gauge in determining how much you’re comfortable keeping in riskier assets like stocks versus less risky investments, like high-quality bonds and cash. “The goal is to understand how much risk you truly can withstand and still sleep at night,” says Mukherjee. That’s your “risk tolerance.”“Markets can change very quickly and unexpectedly, and we cannot control that. What we can control is how we manage risk”

—Niladri Mukherjee, head of CIO Portfolio Strategy, Chief Investment Office, Merrill and Bank of America Private Bank

You’ll also want to determine how much risk you can afford to take with your investments without jeopardizing your goals. Consider things like your income and overall financial resources, along with how much time you have for reaching your goals.

For example, an investor who is within a few years of retirement might avoid putting a large percentage of her net worth into high-risk investments, because the time frame for when she’ll need to access them is shorter than someone with several decades until retirement. Your advisor can work with you to help you get a solid grasp of both your tolerance and capacity for risk.

By sticking within your comfort zone, you’ll be less tempted to abandon the markets when they get volatile — a decision that could hurt your investment returns over time.

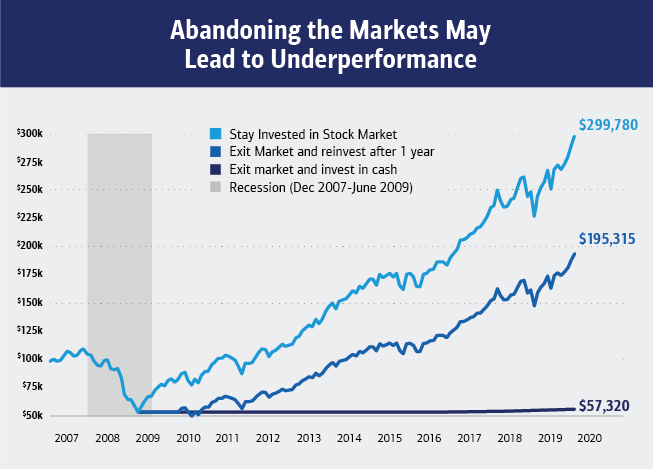

As the graphic below illustrates, an investor who pulled out of the stock market during the Great Recession of 2008 – 2009 and re-invested just one year later would have missed the initial market rebound — significantly reducing their potential returns over the next decade. And someone who exited the stock market and moved their investments into cash would have risked not realizing any returns in the following years.

Past performance is no guarantee of future results. This is for illustrative purpose only and not indicative of any investment. An investment cannot be made directly in an index ©Morningstar. All Rights Reserved.

Another useful strategy, especially if you’re young or new to investing, can be to make a commitment to invest a certain amount on a pre-determined basis — known as dollar-cost averaging. “It can help reduce the urge to try to time the market,” notes Mukherjee, “or make knee-jerk reactions when markets get turbulent.” Keep in mind that dollar-cost averaging cannot guarantee a profit or prevent a loss. And because an investment plan of this nature involves continually investing in securities regardless of fluctuating price levels, you should consider whether you’d be willing to continue purchasing during periods of high or low prices.

What’s the time frame for your various goals?

It’s often helpful to think about the amount of time you have to reach each of your goals, as that will help inform the investment choices you make. Funds to cover unexpected expenses like large home repairs or medical bills or to weather a layoff should be in cash or a highly liquid, low-risk investment such as short-term bonds. For near-term goals that are five or so years away, such as a home down payment, you might opt for conservative investments that typically aren’t as volatile as stocks.

When it comes to long-term goals like retirement, however, being too conservative increases the risk that your portfolio might not grow at a pace that keeps up with inflation. Since 2009, inflation has been low — less than 2% a year. But even a 2% annualized inflation rate means that what costs you $100 today will cost nearly $150 in 20 years, and the purchasing power of your current savings will fall accordingly.

Planning around the corrosive effect of inflation is especially important for your retirement security, given that a non-smoker who reaches age 65 in average health has a 50% probability of still being alive into their mid-80s, and living into one’s 90s is no longer that uncommon.1 So if you have many years before retirement, you could consider a larger allocation to equities that offer greater potential for growth for your longer-term goals, Mukherjee suggests.

You also could consider alternative investments such as private equity funds, if appropriate for your situation. They are often riskier — and less liquid than stocks — but may offer the possibility of higher returns. Your advisor can help determine if these types of investments are appropriate for your circumstances.“An investing strategy that is grounded in your life priorities, goals and time horizon and takes your liquidity needs and risk tolerance into account is the best way to help stay on track and determine if you are making progress.”

—Niladri Mukherjee, head of CIO Portfolio Strategy, Chief Investment Office, Merrill and Bank of America Private Bank

Are there any special situations that might affect your ability to take risk?

The stability of your income might affect how much risk you can take with your investments. Similarly, if you own your own business or have a lot of equity in your employer’s company, you may want to take less risk with your outside investments as a result.

Also take into account significant life changes, such as marriage, divorce, birth of children (and grandchildren), a job loss or new job. “Your risk tolerance is dynamic,” says Mukherjee. “If building more near-term security is a priority, you may want to increase your lower-risk investments for a period, which may entail scaling back riskier assets for longer-term goals, such as saving for future college costs.”

Working through all those moving pieces, with guidance from your advisor, can help you build an over-arching allocation of different types of stocks and bonds, periodically rebalanced to ensure that it doesn’t stray too far from your predetermined allocation — and level of risk. “An investing strategy that is grounded in your life priorities, goals and time horizon and takes your liquidity needs and risk tolerance into account is the best way to help stay on track and determine if you are making progress,” says Mukherjee.

1 Source: Society of Actuaries, June 2020

Important Disclosures

Opinions are as of 11/30/2021 and are subject to change.

Investing involves risk including possible loss of principal. Past performance is no guarantee of future results.

The Chief Investment Office (CIO) provides thought leadership on wealth management, investment strategy and global markets; portfolio management solutions; due diligence; and solutions oversight and data analytics. CIO viewpoints are developed for Bank of America Private Bank, a division of Bank of America, N.A., (“Bank of America”) and Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S” or “Merrill”), a registered broker-dealer, registered investment adviser and a wholly owned subsidiary of Bank of America Corporation (“BofA Corp.”). This information should not be construed as investment advice and is subject to change. It is provided for informational purposes only and is not intended to be either a specific offer by Bank of America, Merrill or any affiliate to sell or provide, or a specific invitation for a consumer to apply for, any particular retail financial product or service that may be available.

Investments have varying degrees of risk. Some of the risks involved with equity securities include the possibility that the value of the stocks may fluctuate in response to events specific to the companies or markets, as well as economic, political or social events in the U.S. or abroad. Bonds are subject to interest rate, inflation and credit risks.

Strategic allocations are hypothetical and are not intended to indicate specific investment recommendations or advice. Asset allocation cannot eliminate the risk of fluctuating prices and uncertain returns, and does not ensure a profit or protect against loss in declining markets.

Risk management and due diligence processes seek to mitigate, but cannot eliminate risk, nor do they imply low risk.

Alternative Investments are speculative and involve a high degree of risk.

Alternative investments are intended for qualified investors only. Alternative Investments such as derivatives, hedge funds, private equity funds, and funds of funds can result in higher return potential but also higher loss potential. Changes in economic conditions or other circumstances may adversely affect your investments. Before you invest in alternative investments, you should consider your overall financial situation, how much money you have to invest, your need for liquidity and your tolerance for risk.